Business Confidence Remains Weak Amid Slowing Growth & Rising Trade Tensions

- The current state of trade war between the US and China, and the resulting impact on global economic growth, has negatively impacted demand, business confidence and commodity prices.

- There is a lot of uncertainty in business planning, due to rising protectionism across economies and trade frictions between US and China.

- Although the Chinese economy showed some positive signs of improvement in the first quarter of 2019, but with April and May figures coming in, the data shows that the momentum remains weak.

- US economy too has witnessed a slowdown in growth, with manufacturing PMI at 50.6 in May 2019, the lowest level in over 9 years.

- The world is more connected now than before, and if we see signs of more economic trouble in China and the US, the global economy is likely to face downside risks to economic growth.

- Steel prices in the US have declined sharply, at a time when iron ore and coking coal prices are rising. Tight high grade iron ore supplies and higher steel production in China is supporting iron ore prices and other steel making raw materials.

The Current State of Trade War Remains a Cause of Concern

- Recent comments from the US President indicate that the two countries are far from a deal.

- Dashing hopes of a quick agreement on trade relations with China, US President Donald Trump’s administration has increased tariffs on $200 billion worth of Chinese goods from 10% to 25%.

- The Chinese government has responded with new tariffs on $60 billion of US products. Trump, meanwhile, has begun the process of expanding U.S. tariffs to cover all $540 billion worth of Chinese imports, which could potentially be a big jolt to the global economic and business sentiment.

- US President Trump announced on Thursday that the US will impose a 5% tariff on all Mexican goods starting from June 10th and warned that it could rise as much as 25% until the country stops the flow of illegal immigrants.

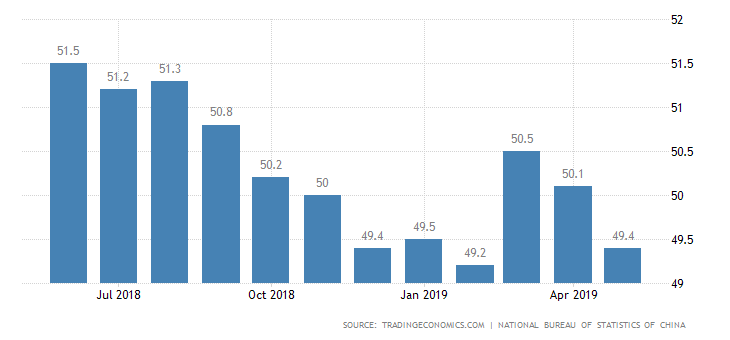

The Momentum in Chinese Economy Remains Weak Despite Stimulus Measures

China NBS Manufacturing PMI

- There have also been several rounds of stimulus measures undertaken by the Chinese government in the past 6-8 months, with talks of several more.

- Although the Chinese economy showed some positive signs of improvement in the first quarter of 2019, but with April and May figures coming in, the data shows that the momentum remains weak. The Chinese economy has witnessed contraction in manufacturing growth in 3 out of the past 5 months. The official manufacturing PMI fell to 49.4 points in May 2019, below the 49.9 level expected by economists, on account of lower export orders.

- Chinese government stimulus measures have remained short lived, as the overall sentiment and business confidence is weak.

US Economy Too has Seen Slowing Economic Growth

US economy too has seen slowing economic growth, with manufacturing PMI at 50.6 in May, more than 9-year low. The IHS Markit US Manufacturing PMI dropped to 50.6 in May 2019 from the previous month’s 52.6 and below market expectations of 52.5, a preliminary estimate showed. The latest reading pointed to the weakest pace of expansion in the manufacturing sector since September 2009.

US Manufacturing PMI Chart, Source: Tradingeconomics.com

- Rising tariffs would are likely to increase costs for consumer goods, and in the US if the consumer is not happy, the economy may face challenges.

Higher Steel Production & Supply Problems Drive Raw Material Prices Higher

- The movement in Chinese steel prices generally has its impact on steel prices across the globe, as the country is the biggest steel producer, consumer, and exporter.

- Steel demand and production in China has remained strong, amid a slew of stimulus measures undertaken by the Chinese government. As a result of increased demand from Chinese steel companies, iron ore port inventories have been shrinking, leading to a big spike in iron ore prices in the past few months.

- 62% Fe Iron ore fines prices have increased from an average of $70/ton at the start of the year to reach around $98. China’s April steel production totaled 85.03 million tons, which represented growth of 12.7% month-over-month and 11% YoY. Between January and April 2019, China produced ~312 million tons of steel, implying an increase of 10.1% YoY.

- While, steel production has increased and raw material prices have also risen, weak demand has prevented producers to increasing finished steel prices, leading to lower profit margins.

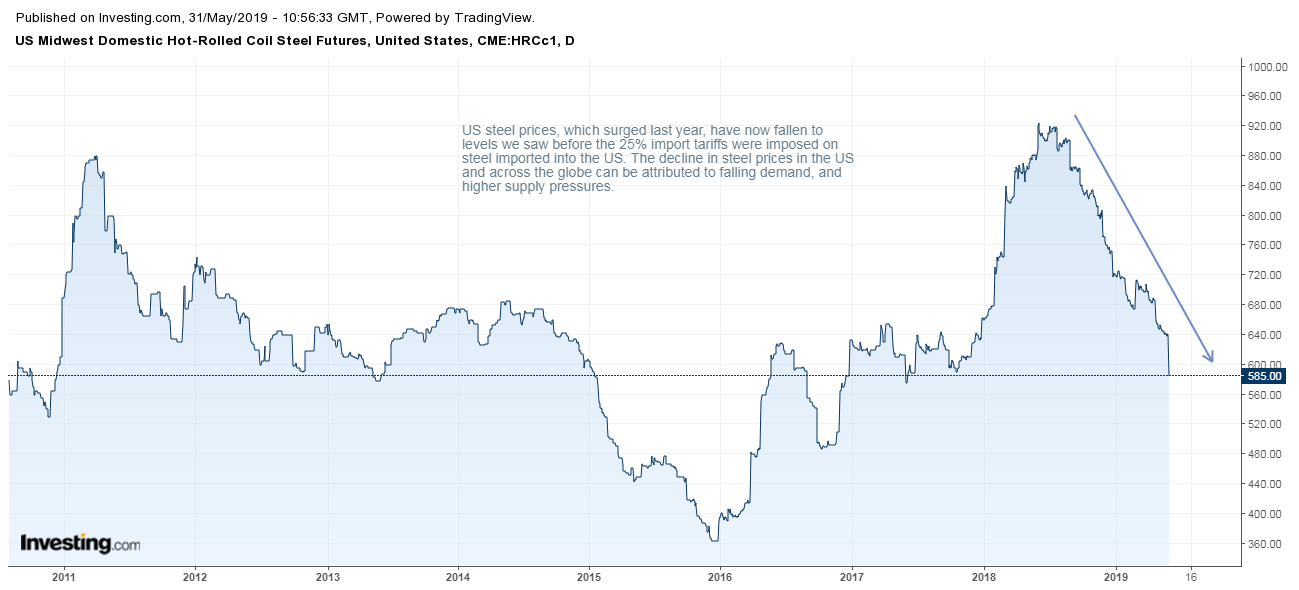

- In the US, steel prices which rose last year, have now fallen to levels we saw before the 25% import tariffs were imposed on steel imported into the US. The decline in steel prices in the US and across the globe can be attributed to falling demand, and higher supply pressures.

US Midwest Domestic Hot-Rolled Coil Steel Futures – (HRCc1)

While, Base Metal Prices have been negatively Impacted amid Trade War Concerns

Copper prices at US$5830/ton are currently trading at a very big support. The current long term up trend support from 2016 low – stood at $5800/ton levels. If prices remain below this level for a while, we could see a sharp decline in prices to $5500, followed by $5050 levels. Weak manufacturing data from the US and China, in addition to rising trade tensions have negatively impacted copper and other base metal prices such as aluminium.

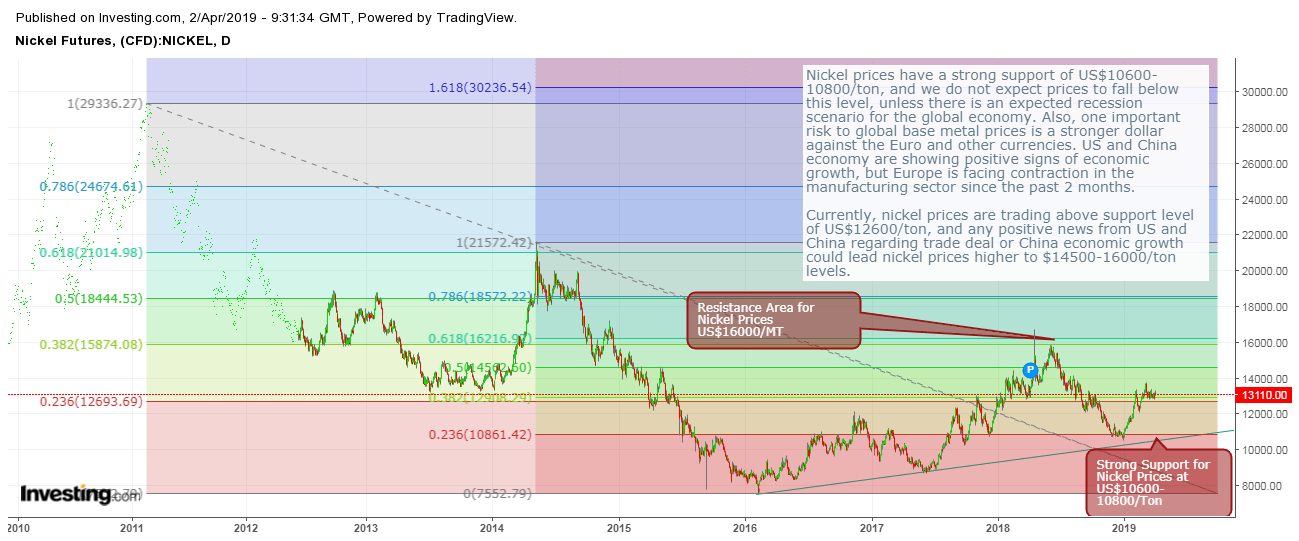

Nickel Prices remain Resilient on Rising Demand from EV Battery Manufacturers

Nickel prices have strong technical support in US$10500-US$11,000 levels. On the fundamental front falling inventories and rising demand for high grade nickel from the battery manufacturers could lead to higher prices. Any fall in nickel price, should be taken as an opportunity buy by physical metal investors and businesses.

Currently, at US$12100/ton levels nickel is moving between strong long term downtrend line resistance from 2014 high at US$14000-US$14500/ton and strong long term support line from 2016 year low at US$10500-US$11000. Nickel prices await positive news on the economic front.

- The total nickel inventory monitored by LME stood at 160290 tons, on 30th May 2019. Last time when nickel inventories stood at this level LME nickel price was US$16,700.

- The cancelled warrants ratio (metal earmarked for delivery) stood at 35.7% on 29th May 2019, down from 40.4% as on 8th May 2019, but up from ~25% at the start of this year.

- The average daily decline in nickel inventories in May 2019 stood at 425 tons, up from 306 tons in April.

- Any positive news on trade war front or on economic growth in China, would lead the prices higher. We do not expect nickel to break the long term support line, on the back of falling inventories and expectations for strong demand in coming years.

Short Term Outlook

- For every business, especially dealing with the US and China, or involved in some type of commodity – the level of uncertainty has been very high. The best of the business managers, can’t take decisions in such atmosphere.

- In the past 1 year we have seen, businesses across the globe has expressed concerns over the future direction of the global economy. If a trade deal is not reached, the downside risks to global economic growth would increase. Even if a trade deal is reached, there would be compromises at both ends and the economic impact of the same would also be negative over the short term, but comparatively lower.

- These days whenever we see weak economic data in China, financial markets do not react much on expectations that there would be additional fiscal and monetary stimulus. This cannot continue forever, and one day we will see the financial markets realize that the trade war and its impact on the Chinese and US economy could be much bigger than expected. Fiscal and stimulus measures take time to reach the direct consumers and businesses. Consumers and businesses completely rely on the future prospects for their spending and investment activities and since the trade war has started, the vision is everything but clear.

- Generally April, May and June are weak for commodity prices, owing to lower demand. Additionally, rising trade tensions makes us believe that base metals and commodity prices would remain weak, unless a trade deal is reached. The exception to this would be steel prices and nickel prices. Steel prices have been supported by rising raw material prices, while in case of nickel technically there is strong price support around US$10500-11,500.

The Author – Metline Industries is a leading manufacturer and processor of aluminium, nickel, titanium and stainless steel alloys in various forms including pipes, plates, fittings, flanges, and relate piping accessories. We are India’s leading steel pipes supplier and steel plate suppliers, with exports to over 50 countries worldwide. Our key products include stainless steel plates, stainless steel sheets, aluminium plates, aluminium sheets, stainless steel coils, stainless steel pipes, stainless steel pipe fittings, stainless steel round bars, stainless steel angles, flexible hose pipes, ss flexible hose pipes and stainless steel flanges. We are India’s leading pipes fittings manufacturer with exports to the US, Europe, Saudi Arabia, Qatar, Kuwait, and various other Middle East Nations.

Leave A Comment